Powell Speaks Soon: Here Are 3 Ways to Hedge Gains

Can Semiconductor Stocks Withstand an Oil Shock?

Semiconductors have led stocks higher since the AI rally began, but they may face new risks as oil prices jump.

Call toll-free 800.328.1267

Federal Reserve news this week could trigger volatility. This article will consider three potential hedging strategies before the events.

First, here are the potential catalysts:

The basic question is how aggressively the Fed will cut interest rates over the remainder of 2025. Futures pricing tracked by CME’s FedWatch tool shows the market expecting a 25 basis-point cut on September 17 and at least one more in October or December.

However, last week’s inflation readings were higher than policymakers’ target. Initial jobless claims also show a relatively tight labor market. Those points could potentially argue against aggressive rate cuts.

Traders worried about volatility can use various option strategies. Here are three potential approaches they may consider:

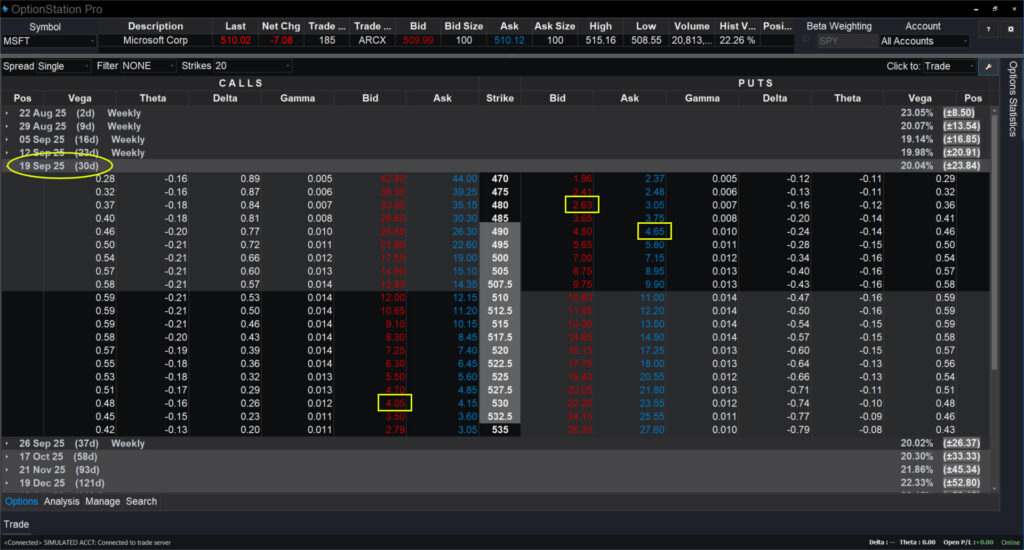

OptionStation Pro, highlighting Microsoft (MSFT) contracts cited in this article.

Puts often gain value when stocks fall because they fix the price where a security can be sold. Traders can also combine long and short legs in a vertical spread to leverage a move between two prices.

For example, Microsoft (MSFT) has drifted lower after hitting a record high above $550 late last month. It closed yesterday at $509.77. Investors worried about more downside could:

Such a trade would cost about $2. It would expand to $10 if MSFT closes at $480 or lower on expiration. That’s a potential gain of roughly 400 percent from the stock dropping 6 percent. The position will expire worthless if MSFT remains above $490.

Vertical spreads have another drawback: Maximum gains occur at the the lower strike, so moves below $480 won’t make any additional profit.

Say an investor purchased 100 shares of MSFT before its recent rally and is now sitting on big gains. He or she could hedge with a “collar” strategy:

Such a trade would cost $0.60 per share, or $60 in total. Because the investor owns stock, they can sell calls against the equity to collect a credit. That cash can then be used to buy puts with the potential to gain value if prices fall. The collar will expire worthless if MSFT remains between $490 and $530.

Investors might recognize some key differences between vertical spreads and collars.

Cost:

Assignment risk:

Profit to the Downside:

Upside Exposure:

In other words, collars are “cheaper” because they surrender future potential profits to protect against potential downside. Spreads cost more, but “keep you invested.”

Invesco QQQ (QQQ), daily chart, showing implied volatility.

Another alternative is to buy puts on an exchange-traded fund (ETF) like the Invesco QQQ Trust (QQQ), which tracks the Nasdaq-100.

Traders can potentially buy vertical put spreads on QQQ if they expect the broader market to decline.

They might also consider long-dated puts that are far out of the money. These contracts tend to have higher Vega, which makes them sensitive to potential spikes in volatility. (See this article for more on option Greeks like Vega and Delta.)

For example, QQQ’s 18-September 2026 250 puts have 0.23 Vega and cost about $1.65. They will gain about $0.23 for every 1 percentage point that implied volatility (IV) increases on QQQ.

This strategy essentially isolates volatility for investors to trade. It can potentially make sense when volatility is near the bottom of its long-term range, as it now is. (See the chart.) For example, if IV climbs from roughly 20 to 30 percent, the puts cited above could gain about $2.30 — more than doubling.

While other strategies can make more money from such a drop, long-dated puts have other potential benefits:

In conclusion, investors may think they don’t need to hedge when volatility is low. But such moments can also make protective strategies more affordable. Trades like vertical spreads, collars, and long-dated puts each have unique costs, benefits and risks. Investors should consider these trade-offs to understand whether a given strategy works and aligns with their goals and risk tolerance.

| ETF | 1 Year | 5 Years | 10 Years |

| Invesco QQQ (QQQ) | +19.94% | +112.75% | +405.69% |

| As of July 31, 2025. Based on TradeStation data | |||

Exchange Traded Funds (“ETFs”) are subject to management fees and other expenses. Before making investment decisions, investors should carefully read information found in the prospectus or summary prospectus, if available, including investment objectives, risks, charges, and expenses. Click here to find the prospectus.

Performance data shown reflects past performance and is no guarantee of future performance. The information provided is not meant to predict or project the performance of a specific investment or investment strategy and current performance may be lower or higher than the performance data shown. Accordingly, this information should not be relied upon when making an investment decision.

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com/DisclosureOptions. Visit www.TradeStation.com/Pricing for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

Semiconductors have led stocks higher since the AI rally began, but they may face new risks as oil prices jump.

After a long bidding war for Warner Bros. Discovery, one big options trader is looking for the current deal to go through.

Explore how FuturesPlus supports futures spread trading with tools for product discovery, advanced filtering, MD Trader execution, Spread Matrix visualization, and custom spread construction using Auto Spreader. Review how to analyze and manage both exchange-listed and synthetic spreads within a structured trading workflow.