Chipmaker Breakout or Oil Shock?

Call Volume Spikes: Has Oracle Bottomed?

Is Oracle finally bottoming? Some traders may think it has.

Call toll-free 800.328.1267

Chipmakers are trying to break out as investors brace for a potential oil shock.

The Philadelphia Semiconductor Index surged 13 percent to a new record high last week. It was the index’s biggest gain since late 2022, fueled by several positive headlines related to AI data centers.

Intel (INTC) jumped after Wired reported it may provide chip-packaging services to Amazon.com (AMZN) and Alphabet (GOOGL). It’s also working with Elon Musk’s Terafab foundry project and GOOGL on chip design. That resulted in INTC’s biggest weekly gain since early 2000.

Broadcom (AVGO) rose to its highest level since mid-December after signing contracts with GOOGL and Anthropic.

Taiwan Semiconductor (TSM) had its best week in almost a year after announcing strong March sales. Its earnings are due Thursday morning.

| Intel (INTC) | +24% |

| SanDisk (SNDK) | +21% |

| Monolithic Power (MPWR) | +21% |

| Lam Research (LRCX) | +21% |

| Coherent (COHR) | +19% |

| Source: TradeStation data |

CoreWeave (CRWV) signed a multiyear data-center deal to provide computing power to Anthropic. That helped ease worries about a company that’s borrowed heavily to build infrastructure.

South Korea’s Samsung preannounced strong results on demand for AI chips. SK Hynix also jumped. Both companies are closely associated with the American AI boom. The country’s KOSPI index surged 9 percent, its biggest weekly gain since early 2021.

Tensions in the Persian Gulf have continued to worsen despite positive momentum in AI stocks. President Trump threatened to blockade Iranian exports starting at 10 a.m. ET today. The move followed unsuccessful peace talks in Pakistan and an attempted ceasefire last week.

The war remains a major risk for markets as energy shortages worsen and prices climb. Crude oil futures jumped 9-10 percent last night, following a month of consolidation.

Higher energy costs are also driving inflation. Last month’s consumer-price index jumped 3.3 percent year-over-year, its biggest increase in almost two years. The market has mostly looked past the spike and hoped for an end to the Iran war. But investors may get more concerned about interest rates if prices don’t fall soon.

Minutes from the Federal Reserve meeting also showed policymakers are concerned about the impact of the conflict. Some officials want to start discussing the potential need for rate hikes.

Consumer sentiment fell more than expected to a new all-time low. It also resulted from anxieties about inflation and the war.

Some experts fear the Iran crisis will get harder to resolve the longer it lasts. That could make it become a greater risk for stocks going forward, but also increase chances of a rally if tensions ease.

| Akamai Technologies (AKAM) | -23% |

| ServiceNow (NOW) | -19% |

| Intuit (INTU) | -17% |

| Axon Enterprise (AXON) | -16% |

| Fair Isaac (FICO) | -15% |

| Source: TradeStation data |

The top 10 gainers in the S&P 500 last week benefit from data centers and AI. Some, like INTC and SanDisk (SNDK), provide chips. Others like Lam Research (LRCX) and Teradyne (TER) sell equipment for making chips. Coherent (COHR) jumped after announcing improvements to its fiber-optic technology for data centers. Corning (GLW) also rallied but didn’t make the top 10.

Nebius (NBIS), which builds and runs AI data centers, broke out to a new all-time high. Some industrial companies like Comfort Systems USA (FIX) and Carrier (CARR), which help cool data centers, also jumped.

Something potentially important happened in Nvidia (NVDA) and AVGO, the two biggest chipmakers. Both had been drifting for months and started last week under their 200-day moving averages. But they rallied sharply and ended the week above their recent ranges. Both companies also had strong earnings in their most recent reports. Given the other positive AI news, are these two important stocks starting to move again?

Those companies mostly provide physical infrastructure for AI. In contrast, software companies continued to slide on worries AI will hurt their businesses.

Akamai Technologies (AKAM) plunged on worries that Claude Managed Agents will hurt its content and infrastructure businesses. ServiceNow (NOW) had its worst week in a decade after getting downgraded by UBS. Cybersecurity companies fell on worries about competition from Claude Mythos. Palantir Technologies (PLTR) fell after Michael Burry said it may face competitive threats from Anthropic.

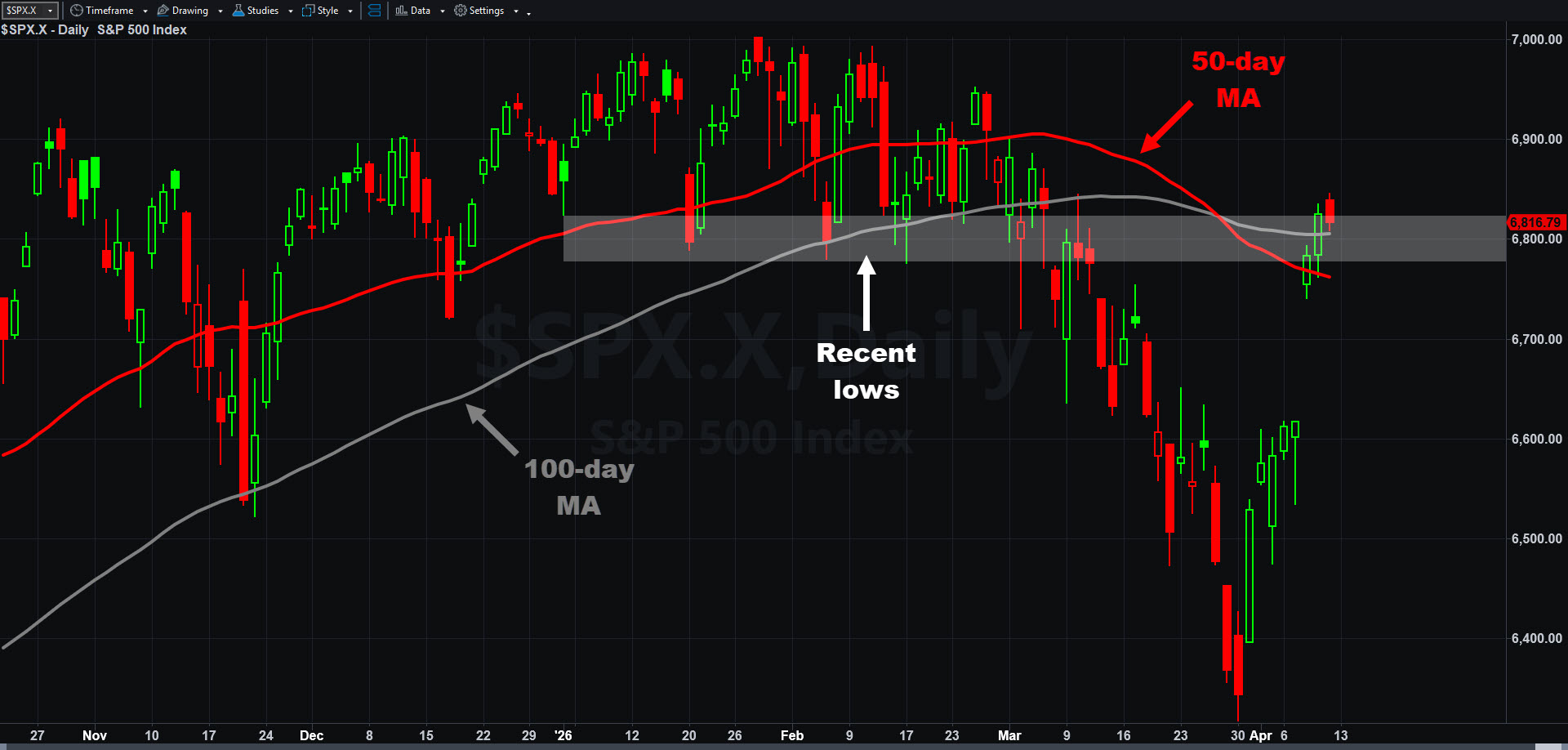

The S&P 500 climbed 3.6 percent last week, its biggest gain since November. President Trump’s call for a ceasefire drove most of the surge.

The index is back in a range above 6,800 where it bounced several times in January and February. Traders may expect the status of the war to influence its direction. Failure to reopen the Strait of Hormuz could slow the advance and turn the old support into resistance. Resolution of the conflict could result in a breakout and advance to new highs.

Regardless, some chart watchers may think the index was overbought in the near term and expect a pause before its direction becomes clear.

S&P 500, daily chart, with select patterns and indicators.

News about the Iran conflict is likely to remain important in the coming sessions. This week also brings first big set of earnings reports and some economic data.

Existing home sales are this morning, along with results from Goldman Sachs (GS).

JPMorgan Chase (JPM), Citigroup (C) and Wells Fargo (WFC) report tomorrow. The producer price index (PPI) is also due.

Wednesday features crude oil inventories and NAHB’s homebuilder index. Bank of America (BAC) and Morgan Stanley (MS) report.

Thursday brings initial jobless claims and results from TSM and Netflix (NFLX).

Is Oracle finally bottoming? Some traders may think it has.

Stocks face big tests as investors watch for signs of the Hormuz crisis improving.

Transocean began the year with a steady rally. Now, after a brief period of consolidation, some traders may expect further gains.