Jade lizard options strategy: from strike selection to fill

Netflix Falters as AI Lifts Other Stocks

Netflix has struggled as AI trades dominate the market. Is the long-term growth stock finally stalling?

Call toll-free 800.328.1267

You’ve got the setup. IV rank at 62. Neutral-to-bullish thesis. The math works on paper.

Then you start clicking.

Three legs. One rule. Total credit from the short put, short call, and long call protection has to exceed the call spread width. Clear that condition, and your upside risk at expiration goes to zero. Miss it, and you just entered a trade with defined risk on both sides.

You sell the put. Filled at $1.60. You move to the call side and short the 20-delta call at $0.70. The chart starts moving. You click to buy the $2-higher long call for protection, but the underlying’s ticked up and the debit has jumped from $0.25 to $0.45. Your total credit came in at $1.85 against a $2.00 call spread width.

You’re fifteen cents short.

You built the jade lizard. You just built the wrong one. The trade you modeled an hour ago has little to do with the trade now sitting in your account.

This is the execution friction on complex premium-selling: the cost of executing a three-leg structure through a one-leg interface.

You understand the jade lizard. You sell an OTM put (typically cash-secured), sell an OTM call, and buy a further OTM call for protection. You collect a net credit. If the total credit exceeds the call spread width, the call side produces a profit at expiration even if the underlying runs well above both call strikes. The remaining risk sits on the short put. Your downside breakeven at expiration is the short put strike minus the total credit. Loss grows from there as the underlying falls further, with maximum loss realized if the underlying goes to zero.

You’ve done the math.

But your platform treats each leg as a separate event. You’re building a structure whose entire value proposition depends on a credit condition, through a workflow that makes it harder to hit that condition with every click.

TITAN X treats multi-leg spreads as single orders from the start. You build the structure, verify the credit condition, check the Greeks, and submit once. Here’s the workflow.

You’ve already identified the candidate using TradingView for technical analysis, one of TradeStation’s third-party partners. The chart shows price consolidating above support over the past two weeks, with no earnings or major catalysts inside your expiration window.

For IV analysis across your universe, third-party partners like OptionsPlay and ORATS connect to TradeStation and provide IV Rank and IV Percentile scanning. Elevated IV is your trigger: rich premium on the short put makes the credit-exceeds-width condition easier to satisfy.

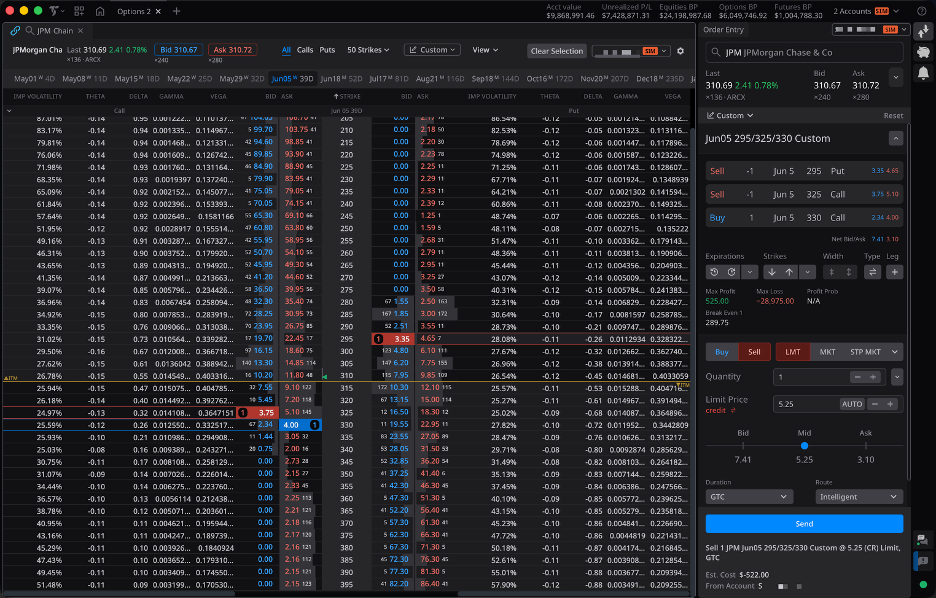

Load the symbol into TITAN X. Click it in your watchlist, and the chart and options chain update simultaneously. No retyping or searching. You’re looking at the options chain in seconds, with implied volatility displayed per strike inline.

Open the spread selector in TITAN X’s options chain. Build your jade lizard across all three legs as a single spread order: sell an OTM put at roughly 20–30 delta (typically cash-secured), sell an OTM call at roughly 15–20 delta, and buy a further OTM call for protection. Call spread width is typically $1 to $5 depending on the underlying and the credit you can collect.

You’re not building this piece by piece. You’re selecting a structure.

Now the critical part. Before you’ve committed anything, TITAN X displays net credit on the trade ticket and real-time Greeks for each leg. From there, you verify the condition yourself: is your total credit greater than the call spread width? If yes, upside risk at expiration is eliminated. If no, you’re entering a trade with defined risk on both sides.

You adjust strikes by clicking different rows. The calculations update in real time. You’re not guessing whether the credit condition holds. You’re modeling it live.

Want a second opinion? TradeStation’s third-party partners like OptionsPlay and ORATS provide strategy comparison and advanced analytics, letting you evaluate this jade lizard against alternatives before committing.

You’ve selected your strikes. The short put is paying $1.60, the bear call spread is netting $0.50 credit, for a total of $2.10 against a $2.00 call spread width. Upside risk at expiration is eliminated. Downside breakeven sits at the short put strike minus $2.10; loss grows from there as the underlying falls further.

Consider setting your limit price at or slightly better than the mid-market price. You see all three legs, the net credit, and the margin requirement.

All three legs route as a single order. Legging risk is significantly reduced. You’re not racing between fills while the credit condition slips away from you.

Want to try it out on TradeStation? Open an account

The position’s live. Theta’s working on two short legs. But markets move, and sometimes the underlying tests your short put.

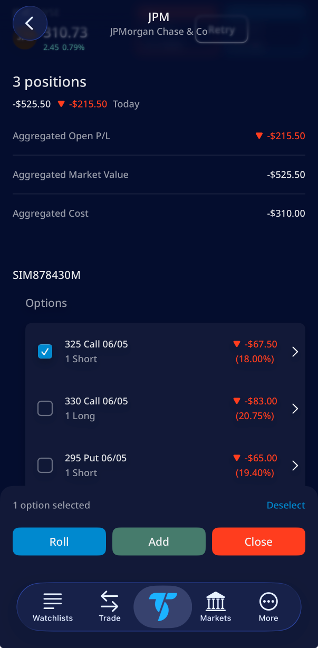

The TradeStation Mobile App gives you comprehensive spread management on the go, including custom multi-leg spread construction, iron condors, and rolling capabilities. The app displays real-time Greeks for each leg and the net position.

If you’ve hit your profit target with three weeks remaining, you can close all three legs from your phone. Tap the position, tap Close, confirm the debit. Capital freed. Risk largely off the table.

If the underlying drops toward your short put, you can roll the spread directly from TradeStation Mobile. Close the current position and open a new one at a lower put strike and a later expiration, ideally for a net credit. You adjust from wherever you are.

Rolling works on TITAN X, mobile, and the classic desktop experience. Same execution engine everywhere.

For traders managing multiple jade lizards across a portfolio, OptionStation® Pro on desktop provides 3D risk graphs and portfolio-level Greeks, including beta-weighted delta views for aggregate directional exposure.

The jade lizard math only works if your total credit exceeds the call spread width. That constrains strike selection more than most three-leg structures.

The short put at 20–30 delta typically provides the bulk of your credit. The bear call spread needs to be wide enough to be worth building but not so wide that the credit-to-width ratio breaks. Typical construction: 15–20 delta short call with the long call $1–$5 above it, depending on the underlying’s price and how much credit the short put contributed.

In elevated IV, you have more room. The short put alone may pay enough that even a $3 or $5 wide call spread can satisfy the credit-exceeds-width condition. In low IV, you’ll typically need a narrower call spread, and less upside headroom, to make the math work.

Both are range-oriented premium-selling strategies. The iron condor caps risk on both sides with four legs. The jade lizard uses three legs and can eliminate upside risk at expiration when the credit exceeds the call spread width.

Consider the jade lizard when your directional bias is neutral-to-bullish and IV is elevated enough that the short put alone generates substantial credit. You’re accepting downside risk in exchange for upside risk eliminated at expiration when the credit condition holds, and simpler construction.

Consider the iron condor when you want defined risk on both sides and you’re comfortable with typically lower credit per contract in exchange for the symmetric protection.

Consider closing at 25–50% of max profit to capture most of the gain while avoiding gamma risk near expiration. The two short legs peak their theta decay in the final weeks, but gamma also accelerates, making mark-to-market P&L more volatile.

If the short put gets tested, the position can often be rolled down and out for additional credit, provided the extended time premium on the new put exceeds the debit to close the current one. On deeply tested positions, rolling may require a net debit or a wider risk profile. Rolling is a defensive move, not a profitable one in isolation. It buys time and collects more premium, but the underlying still has to stabilize for the trade to work.

The jade lizard includes a short put, typically cash-secured, which carries substantial downside risk if the underlying falls sharply. The strategy requires appropriate options approval (generally at least Level 3 for cash-secured puts; higher levels are required if the short put is held on margin rather than cash-secured). If your total credit doesn’t exceed the call spread width, you have defined risk on the upside as well, meaning risk on both sides of the trade instead of only the downside. Early assignment on the short call becomes more likely when it goes deep in the money with little time value remaining, and on dividend-paying stocks around ex-dividend dates. Early assignment on the short put is also possible when it goes deep in the money near expiration. Consider closing positions before expiration if the underlying is near either short strike to help avoid pin risk. Defined risk on the upside doesn’t mean no risk overall.

Build the structure. Verify the condition. Submit once.

Want to learn more? Explore the Options Education Center

Ready to trade? Open a TradeStation account

Trade like you were born to do this.

Disclosure:

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com/DisclosureOptions. Visit www.TradeStation.com/Pricing for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

Equities, equity options, and commodity futures products and services are offered by TradeStation Securities, Inc. (Member NYSE, FINRA, CME and SIPC).

The examples in this article are hypothetical and for educational purposes only. They do not represent actual trades or guarantee future results. Past performance is not indicative of future results.

ID5456161 P10616072548 D0526

Netflix has struggled as AI trades dominate the market. Is the long-term growth stock finally stalling?

The Nasdaq-100 keeps running as the AI boom widens across the technology sector.

You’ve mapped the ratio diagonal, but the picture fractures when you try to model the actual risk.