The calm before the catalyst: a buy straddle strategy for volatility events

AI Stock ‘Stays Cool’ as Iran War Rages

Vertiv has been a quiet beneficiary of the AI boom and now it’s getting noticed.

Call toll-free 800.328.1267

The market is quiet. Too quiet.

Implied volatility is sitting at the floor. The VIX is compressed. The 30-day realized vol on your watchlist is grinding near its 52-week low. But you know what’s coming. The economic calendar says the FOMC meeting is in three days. CPI prints Tuesday morning. Earnings season opens next week.

This is the setup. You’ve seen it before. Buy the straddle when volatility is cheap. Let the event repricing do the heavy lifting. The thesis is textbook: you’re long vega, betting that implied volatility will expand faster than theta can erode your premium.

The math is clear. The timing is right. Now find the trade.

On a standard retail platform, this is where the process breaks down. You open the option chain on your first ticker. You check the IV percentile manually. You compare it to the 30-day historical average in a separate window. You estimate the expected move. You repeat this process for the next ticker. And the next.

Forty-five minutes later, you’ve screened twelve names. You found two candidates. But, by the time you pull up the second one to size the position, the premium has ticked up 8%. Someone else found it first. The cheap vol isn’t cheap anymore.

You were right about the catalyst. You were right about the direction of volatility. But you couldn’t process the opportunity fast enough to capture it.

You don’t have a thesis problem. You have a throughput problem.

When you trade directional momentum, you compete on speed of entry. When you trade volatility, you compete on speed of discovery. The edge in a pre-event straddle isn’t knowing that CPI will move the market. Everyone knows that. The edge is finding the instrument where the market has underpriced that move.

That requires scanning power. It requires the ability to compare implied volatility across your entire universe in seconds, not minutes. It requires modeling the straddle’s payoff against different volatility expansion scenarios before you commit the capital.

If your platform forces you to check IV one ticker at a time, you’re paying a “retail tax” on every pre-event setup. It’s the cost of bringing a knife to a gunfight – or, in this case, using a telescope when you need a radar system.

TradeStation gives you the radar. The ecosystem of professional options tools helps turn the pre-event volatility hunt from a manual scavenge into a systematic operation: scanning, modeling, and position management designed for the swing trader who lives and dies by the vol cycle.

You don’t find cheap vol by staring at a chart. You find it by letting the data surface the anomalies.

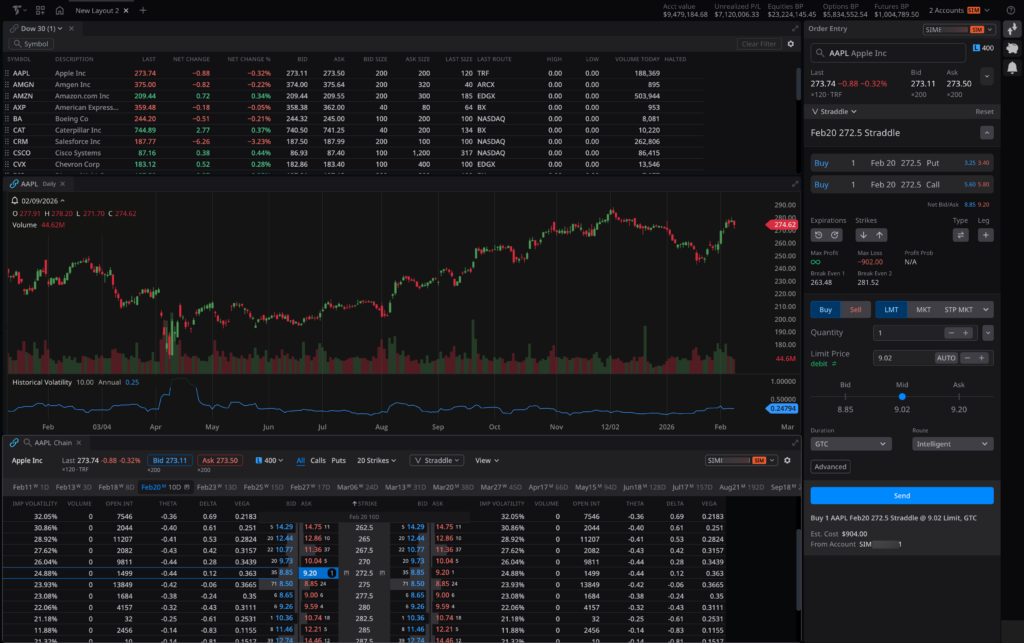

In TITAN X, start with your watchlist. Load your universe; whether it’s 20 large-cap names or 100 high-beta tickers. Link your components so that clicking any symbol in the watchlist instantly updates your charts and options chain in real time. You’re not opening separate windows. You’re cycling through your entire universe with single clicks, scanning IV data directly in the options chain where inline Greeks give you an immediate read on each contract’s pricing.

This visual scanning is fast. It’s how you cut a 100-name universe down to five candidates in minutes.

But for traders running larger universes, TradeStation’s desktop platform takes this further. RadarScreen® lets you track over 1,000 symbols simultaneously with custom columns. Configure it to display your choice of hundreds of pre-built studies and infinite custom indicators or data points of your choosing. When you do this, you don’t hunt for the setup. The setup announces itself.

The boring mid-cap you haven’t checked in weeks? It jumps to the top of the list because earnings are in four days and the IV is historically low. The premium is cheap. The catalyst is confirmed. The opportunity is right there, quantified and ranked, before you’ve taken a second sip of coffee.

So, now you’ve identified the target. The IV is suppressed. The catalyst is confirmed. You still need to answer one question: is this straddle worth the premium?

In TITAN X, select Straddle from the spread selector. Both legs populate instantly and the ATM call and ATM put matched to your selected expiration. The trade ticket displays max loss, breakeven points, and estimated P&L before you send a single order. You know your risk parameters at a glance.

For deeper modeling, OptionStation® Pro on the desktop platform gives you the full laboratory. Load the straddle and open the risk graph. You’re looking at a visual projection of your P&L across every possible price at expiration. But the real power is the “what-if” engine. Slide the volatility input forward. What happens to your position if IV expands 20 points? What if it only moves 10? What if the underlying gaps 3% but IV actually crushes post-event?

You can manipulate the date slider to model theta decay day by day across your holding period. You might find that the weekly straddle gives you a tighter breakeven range with less exposure to time decay than the monthly. Or you might discover that the monthly gives you a second catalyst, perhaps an earning report followed by FOMC, for the same theta cost.

You’re not guessing at breakeven points. You’re stress-testing the trade against multiple future states of the market. When the math supports the edge, you execute.

The straddle is on. The catalyst is two days away. Now the discipline starts.

Pre-event straddles are swing trades. They’re not set-and-forget positions. Theta is decaying your premium every day, and you need IV expansion to outpace that erosion. Your job is to monitor that balance and know exactly when to act.

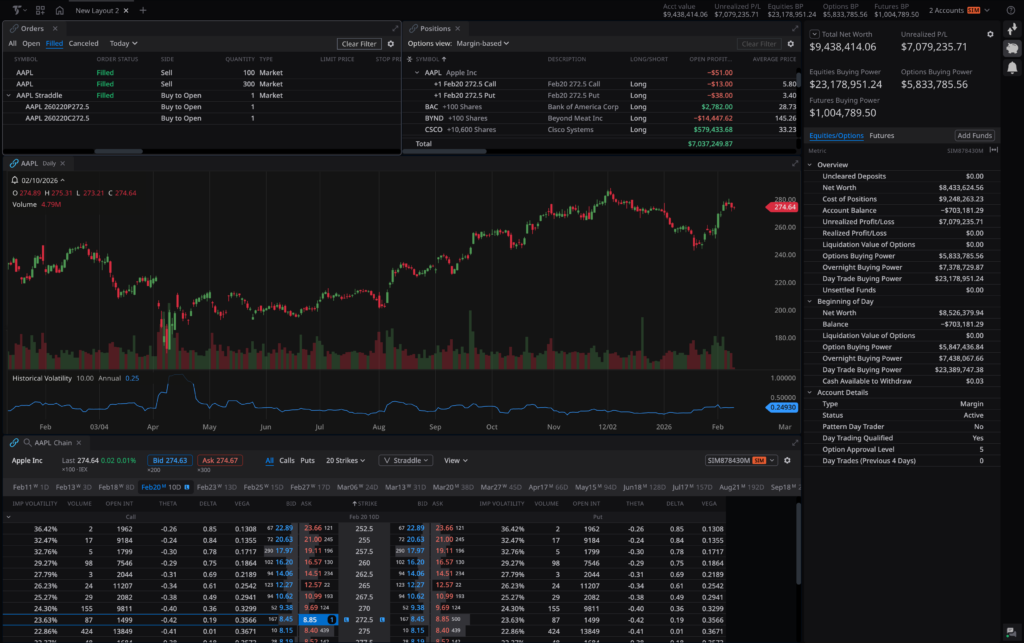

In TITAN X, your positions component groups both legs of the straddle together by symbol. You see unrealized P&L updating in real time. You can sort by profitability to prioritize which positions need attention first.

If the underlying starts to move directionally before the event – a pre-announcement leak, a sector rotation, an analyst upgrade – one leg of your straddle may move significantly into profit while the other decays. This is where management often separates the professional from the passive. You click to close the profitable leg and let the other run. Or you close the entire position if the move has already repriced IV to your target. Or you roll to a new expiration if the initial catalyst has been pushed back.

For portfolio-level monitoring, OptionStation Pro on the desktop tracks aggregate delta and theta across your positions. You know exactly how much more volatility needs to expand to overcome your daily theta bleed.

TradeStation routes your adjustment orders using intelligent order routing technology to seek the best execution available. When you’re managing a straddle in a fast-moving pre-event environment, the quality of your fill on the adjustment can be the difference between a profitable position and a scratch.

Buy straddles are defined-risk positions, but they are not cheap insurance. Theta decay erodes the premium every day, and if the anticipated catalyst produces a muted market response, both legs can expire worthless. The breakeven points on a straddle require a significant move in either direction, and the IV expansion you’re counting on may not materialize if the event fails to surprise the market. Professional scanning and modeling tools help reduce the friction of identifying and analyzing setups, but they cannot eliminate the inherent risk of being long premium. Every straddle carries the possibility of total loss on the position. Approach each trade with clear exit rules and never risk more capital than you can afford to lose.

The next catalyst is already on the calendar. The question isn’t whether the market will move. It’s whether you’ll find the cheapest way to express that thesis before the window closes.

Stop manually scanning option chains for low IV. Stop guessing at breakeven points on the back of an envelope. Stop letting the premium tick away while your platform crawls through your universe one ticker at a time.

Scan for the suppressed volatility. Model the payoff. Execute with precision. Manage the swing with discipline.

Trade like you were born to do this.

Disclosure:

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com/DisclosureOptions. Visit www.TradeStation.com/Pricing for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

Vertiv has been a quiet beneficiary of the AI boom and now it’s getting noticed.

Stocks are whipsawing after the White House suggested it may de-escalate the Iran war.

Volatility is rising as geopolitical and economic risks increase. How will natural born traders react?