Rolling Options: Key Things for Traders to Know

Netflix Falters as AI Lifts Other Stocks

Netflix has struggled as AI trades dominate the market. Is the long-term growth stock finally stalling?

Call toll-free 800.328.1267

“Rolling options” is a common transaction for options traders, but there are several ways to do it. This article will explain the different ways and reasons why traders might roll positions.

These are the key points we’ll cover:

Rolling options is the practice of moving from one call or put to a different call or put on the same stock. It involves exiting the current position and immediately entering a similar position. The underlying stock or exchange-traded fund (ETF) remains the same.

Say an investor bought calls on a stock that subsequently rallies, boosting the value of the calls. He or she could potentially sell their calls and buy others, which would be an example of rolling long calls. The same could be done with long puts.

Trades like this can be executed in a single transaction to lower commissions.

Next, there are several types of options strategies. Investors can be short calls or short puts. In those cases they would roll their options by doing the opposite — buying the short call or put and selling a similar contract.

The purpose of rolling is to adjust an existing position. The new position keeps the same directional bias and structure.

Options are different than stock because they expire and you can’t hold them forever. They either expire worthless or result in a long/short position in the underlying security. Rolling options helps avoid that outcome.

Second, options behave differently based on movements in the stock. Profitable trades often result in calls or puts gaining significant value and moving deep into the money. (For example, an option purchased for $0.50 can appreciate to $5 or more.) While this is good news for the investor, the appreciated option is typically less liquid. (They will also have wider bid/ask spreads.) Rolling options help remedy that situation.

Such appreciated options typically have deltas closer to 1 (or -1 for puts). Traders may adjust their positions by switching to contracts with a lower delta that will initially track the underlier less closely. (This also reduces losses from short-term counter-trend moves.) They’ll receive a net credit in the process.

Time decay is another consideration because options lose value at an accelerating pace as expiration approaches. Selling options with higher absolute theta and buying options with lower absolute theta can help reduce that risk. (Theta is always a negative number.)

Calls fix the level where a security can be purchased. Long calls appreciate when prices rise. Investors sometimes own calls instead of shares because they require less cash. If the stock rallies, the leverage can deliver even greater gains than owning the stock.

They can roll them over time as the shares appreciate, locking in profits along the way and managing time decay.

Puts fix the price where a stock can be sold. They’re the opposite of calls because they appreciate when prices fall.

Investors can use puts to hedge other positions. When expecting a decline in stocks overall, they might buy puts on an ETF like the SPDR S&P 500 ETF (SPY), which tracks the broader market. Traders can also buy puts instead of short selling a stock. (That’s when they look to profit from an expected price decline.)

Either way, puts can gain value as markets move lower. Investors can roll puts the same way they’d roll calls, taking profits and managing time decay. The only difference is that they’d take profits by rolling to lower strikes instead of higher strikes.

A covered call strategy entails holding a minimum of 100 shares and selling (or “writing”) call(s) against them. Investors use this technique when they like a company but want to reduce the risk of owning stock.

The calls sold lose value because of time decay. Therefore, investors can roll covered calls by purchasing the short calls and selling other contracts with later expirations. This may allow them to collect further credits because the longer-dated contracts will have more time value. It can also eliminate the risk of being forced to sell shares if the contracts are in the money.

Rolling a covered call may entail risk by extending the amount of time in a position, during which the underlier can lose value.

Advanced Micro Devices (AMD), daily chart, showing breakout to new highs.

Let’s take Advanced Micro Devices (AMD) as an example given its significant move lately.

Say you had bought the November 200 calls in September, before the most recent surge. At the time, those calls cost about $3.80.

AMD proceeded to rally about 60 percent from percent from that moment. Because the calls have leverage, they inflated more than 1,500 percent. They were bid for $63.55 yesterday.

A trader could have rolled the position by selling the November 200 calls and buying the November 270 calls, offered for $15.25. He or she would have collected a net credit of about $48.30, locking in roughly $44.50 of profit. They’d also stay positioned for more gains if AMD keeps running.

Advanced Micro Devices (AMD) November 200 calls, daily chart.

Those AMD calls have the same expiration date next month. Traders can also extend their time frame by rolling options to a different expiration date.

For example, the trader could have sold the November 200 calls for $63.55 and purchased the December 270 calls for $21.60. That would have generated a credit of $41.95 and locked in a profit of $38.15. It would also provide an additional month for the stock to keep moving.

Next, traders may roll options to adjust covered-call positions.

We’ll use Intel (INTC) as an example. Say an investor purchased 100 shares for $20 in early August. The stock rebounded sharply and was above $30 by late September.

An active trader might have taken advantage of the surge to sell the November 40 calls for about $2.30. INTC consolidated for more than three weeks and those contracts fluctuated between about $1.50 and $3, according to TradeStation data.

OptionStation Pro showing Intel (INTC) calls cited in this article.

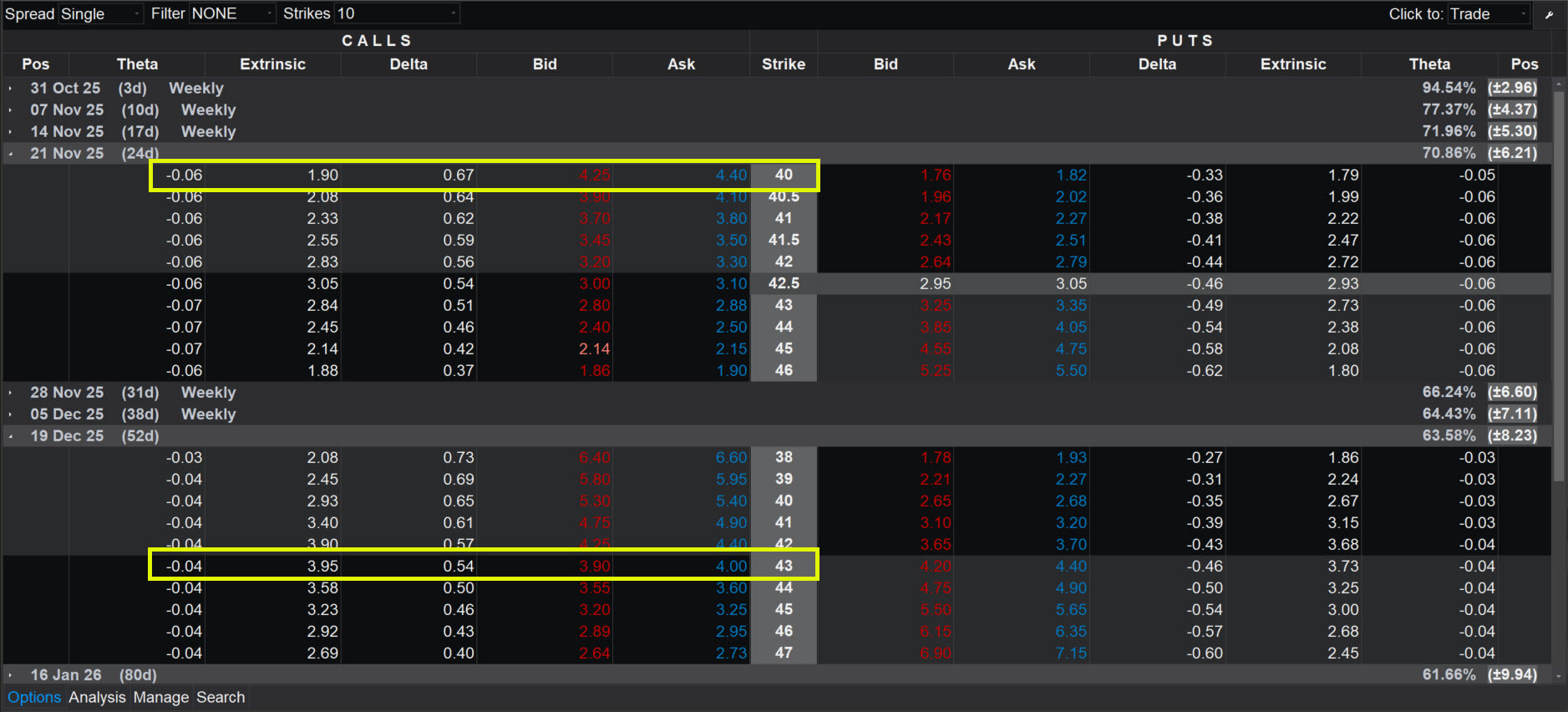

On Tuesday, the stock broke out to a new 52-week high high above $42 and the calls were quoted for about $4.25. They’re now in the money, so the investor cannot profit from any additional upside. Instead, he or she will be forced out of their shares for $40 by expiration on November 21.

They could respond by rolling their position. The November 40s could be purchased for about $4.40 and the December 43 calls could be sold for about $3.90. Making the adjustment would cost about $0.50, and would let them receive an additional $3 on the stock if it continues to advance.

The trader would also buy back calls with $1.90 of extrinsic value, or time value. They would sell calls with $3.95 of extrinsic value, capturing about $2.05 of net premium. That illustrates how covered calls can generate income based on the time value in options.

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com/DisclosureOptions. Visit www.TradeStation.com/Pricing for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

ID4943862 D1025

Netflix has struggled as AI trades dominate the market. Is the long-term growth stock finally stalling?

TradeStation’s platform is known for letting customers build their own tools. It also provides a series of calculated indexes for advanced technical analysis.

You’ve mapped the ratio diagonal, but the picture fractures when you try to model the actual risk.