Bullish, Neutral, Even Bearish: 3 Ways Options Traders Can Use Covered Calls

David Russell

September 21, 2025

Covered calls are one of the most common strategies for options traders. While many investors have heard of them, they may not realize that covered calls are highly versatile. This article will cover how the method can be bullish, neutral and even bearish.

First, a covered call consists of owning shares and selling calls against them. The calls establish a potential obligation to sell stock at a future date, so they need to be married to an existing position in the stock. In most cases, one call contract matches 100 shares.

The nuance results from which strike price the investor chooses to sell. Depending on the contract, his or her position can behave very differently. Here are the three basic variations:

Bullish: Sell calls further from the money

Neutral: Sell calls at the money

Bearish: Sell calls in the money

The examples below use options delta, which indicates how a call behaves relative to changes in an underlying stock. We’ll show how this approach can help investors plan trades in a more systematic fashion. All three cases will use covered calls on Apple (AAPL) as examples, based on Friday’s prices.

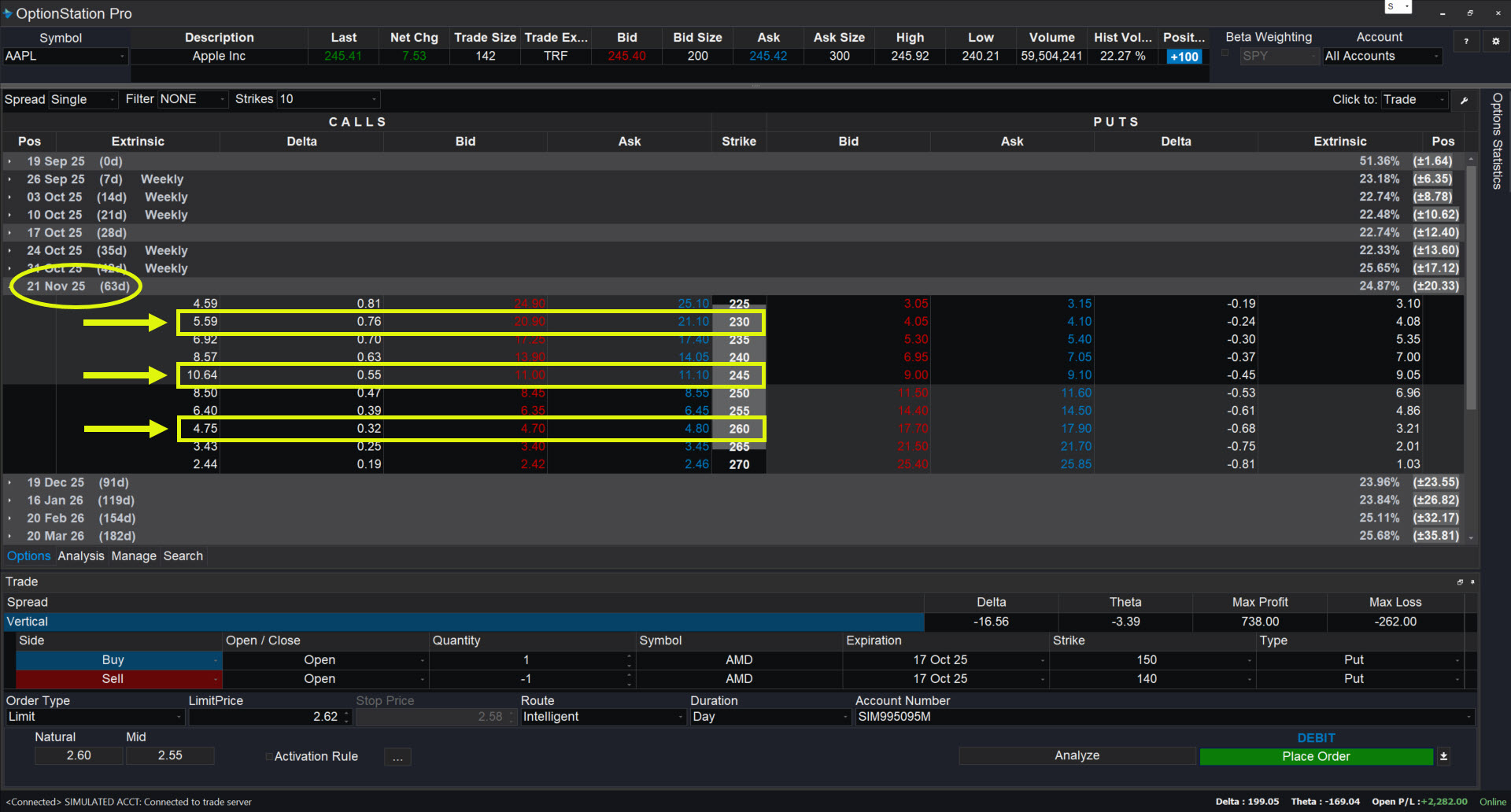

OptionStation Pro showing key Apple (AAPL) contracts cited in this article. Prices as of September 19, 2025.

Covered Call Strategy: Bullish Case

A covered call is most bullish when the trader sells calls further from the money. The reason is that options further from the money have lower delta. That means the short calls offset less of their underlying position.

Say an investor holds 100 shares of AAPL worth $245. If he or she is bullish on the iPhone maker, they could sell a single November 260 call for $4.70. The position’s cost basis would decrease by $4.70 per share thanks to the credit collected.

The November 260 calls have 32 Deltas, which means they gain $0.32 each $1 the stock rises. Because they were sold, the delta is negative. Here’s how it impacts their holding:

100 shares

100 Deltas

1 short call

-32 Deltas

Net position

68 Deltas (68 shares)

This means that the underlying position will now behave like owning 68 shares (not 100). This keeps most of the potential upside intact, while lowering the cost basis by more than 1 percent. This approach lets traders frequently sell calls to generate income while also profiting from the stock rising. The other benefit of this method is that the short calls will lose delta as expiration approaches. That will automatically increase the position’s net delta. In other words, it will become more like 100 shares.

Because the position still has a lot of delta, this strategy’s main risk is downside in the stock price. If AAPL falls sharply, the short calls will do little to offset 100 shares losing value.

Apple (AAPL), daily chart, with 50- and 200-day moving averages. Prices as of September 19, 2025.

Covered Call Strategy: Neutral Case

A covered call is neutral when the trader sells calls near the money because those calls have more delta. They offset more of the underlying position, reducing upside. But they also have more time value, which increases the premium collected.

Again, imagine someone owns 100 AAPL shares worth $245 each. If they’re neutral on the company, they could sell a single November 245 call for $11. The position’s cost basis would decrease by $11 per share thanks to the credit collected.

The November 245 calls have 55 deltas, which means they gain $0.55 each $1 the stock rises. Because they were sold, the delta is negative. Here’s how it impacts the holding:

100 shares

100 Deltas

1 short call

-55 Deltas

Net position

45 Deltas (45 shares)

The underlying position will now behave like owning 45 shares (not 100). This eliminates more than half the upside potential while lowering the cost basis by more than 4 percent. This approach may be suited for times when the stock is expected to move sideways. The premium collected will prevent losing money from a modest drop. But the investor also loses the ability to profit if the shares rally.

This strategy can be repeated after expiration, although in some cases the investor will have to buy back the short call. It mostly capitalizes on the greater time value in options that are closer to the money. (See Extrinsic Value in screen shot.)

Covered Call Strategy: Bearish Case

A covered call is bearish when the trader sells calls deeper in the money because they have significant delta. This can offset the downside in the stock price to a certain point. The strategy can even make small profits from time decay in the options.

Again, imagine an investor has 100 AAPL shares worth $245 each. If they are bearish on the company, he or she could sell a single November 230 call for $20.90. This effectively locks in a selling price of $250.90: 230 strike price + $20.90 credit.

The November 230 calls have 76 deltas, which mean they will lose $0.76 for each $1 that the stock declines. Here’s how it impacts their holding:

100 shares

100 Deltas

1 short call

-76 Deltas

Net position

24 Deltas (24 shares)

The underlying position will initially behave like owning just 24 shares. The correlation will increase to an exact -100 in coming weeks if AAPL remains above $230. The stock can drop more than 6 percent without generating any losses. In fact, the trader may make a small profit because the calls had $5.59 of time value that will decay over the next three months.

This strategy can be useful when investors have made money in a stock and expect a limited pullback. The calls essentially lock in a sale price while extracting some extra time value.

But there’s still risk in the event of a steeper drop. In this case, the investor will lose money if AAPL closes below $209.10 expiration. (That’s the 230 strike minus the $20.90 premium collected.)

Understanding Covered Calls

Options traders should remember that covered calls always generate a credit. That means they get paid now and agree to do something later. (Debit trades are the opposite, costing money now but potentially making money later.)

Performing a covered call will always limit potential profit because the right to own the stock above the strike price has been relinquished. They also provide modest downside protection.

Traders looking for big rallies may want to consider bullish call spreads or owning calls outright. Investors worried about bigger drops could also explore protective puts or bearish vertical spreads.

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com/DisclosureOptions. Visit www.TradeStation.com/Pricing for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

David Russell is Global Head of Market Strategy at TradeStation. Drawing on more than two decades of experience as a financial journalist and analyst, his background includes equities, emerging markets, fixed-income and derivatives. He previously worked at Bloomberg News, CNBC and E*TRADE Financial.

Russell systematically reviews countless global financial headlines and indicators in search of broad tradable trends that present opportunities repeatedly over time. Customers can expect him to keep them apprised of sector leadership, relative strength and the big stories – especially those overlooked by other commentators. He’s also a big fan of generating leverage with options to limit capital at risk.

TradeStation’s platform is known for letting customers build their own tools. It also provides a series of calculated indexes for advanced technical analysis.

For 25 years, four trades in five days could lock you out of your own margin account. That era is ending.

Explore the Crossroads Summit

You are leaving TradeStation.com for CrossroadsSummit.com, an exciting new conference that highlights opportunity at the intersection of chaos and innovation. Click the button below to acknowledge that you understand that you are leaving TradeStation.com.

You are leaving TradeStation.com for another company’s website. Click the button below to acknowledge that you understand that you are leaving TradeStation.com.

This event is hosted on YouCanTrade. The information for this event is being provided for informational and educational purposes only.

You are leaving TradeStation Securities and going to YouCanTrade. YouCanTrade is an online media publication service which provides investment educational content, ideas and demonstrations, and does not provide investment or trading advice, research or recommendations. YouCanTrade is not a licensed financial services company or investment adviser and does not offer brokerage services of any kind.

TradeStation Securities, Inc. provides support and training channels hosted on YouCanTrade, its affiliate. Other than these support and training channels, any services offered by YouCanTrade are not sponsored, endorsed, sold or promoted by TradeStation Securities and it makes no representation regarding any YouCanTrade goods or services.

To acknowledge you are leaving TradeStation Securities to go to YouCanTrade, please click