Vertical spreads are one of the most common strategies in the options market because they can generate leverage with limited risk. This article will consider key points about bullish and bearish spreads.

Vertical spreads involve two “legs” on the same underlier to create a single position:

- One contract near the money is purchased at a higher cost

- For bullish trades, this means a call with a strike above the current stock price.

- For bearish trades, this means a put with a strike below the current stock price.

- Another contract is sold further from the money at a lower cost.

- For bullish trades, this means a call with a strike further above the current stock price

- For bearish trades, this means a put with a strike further below the current stock price

The legs of the vertical spread have the same number of contracts and the same expiration dates.

Example of a Bullish Vertical Spread

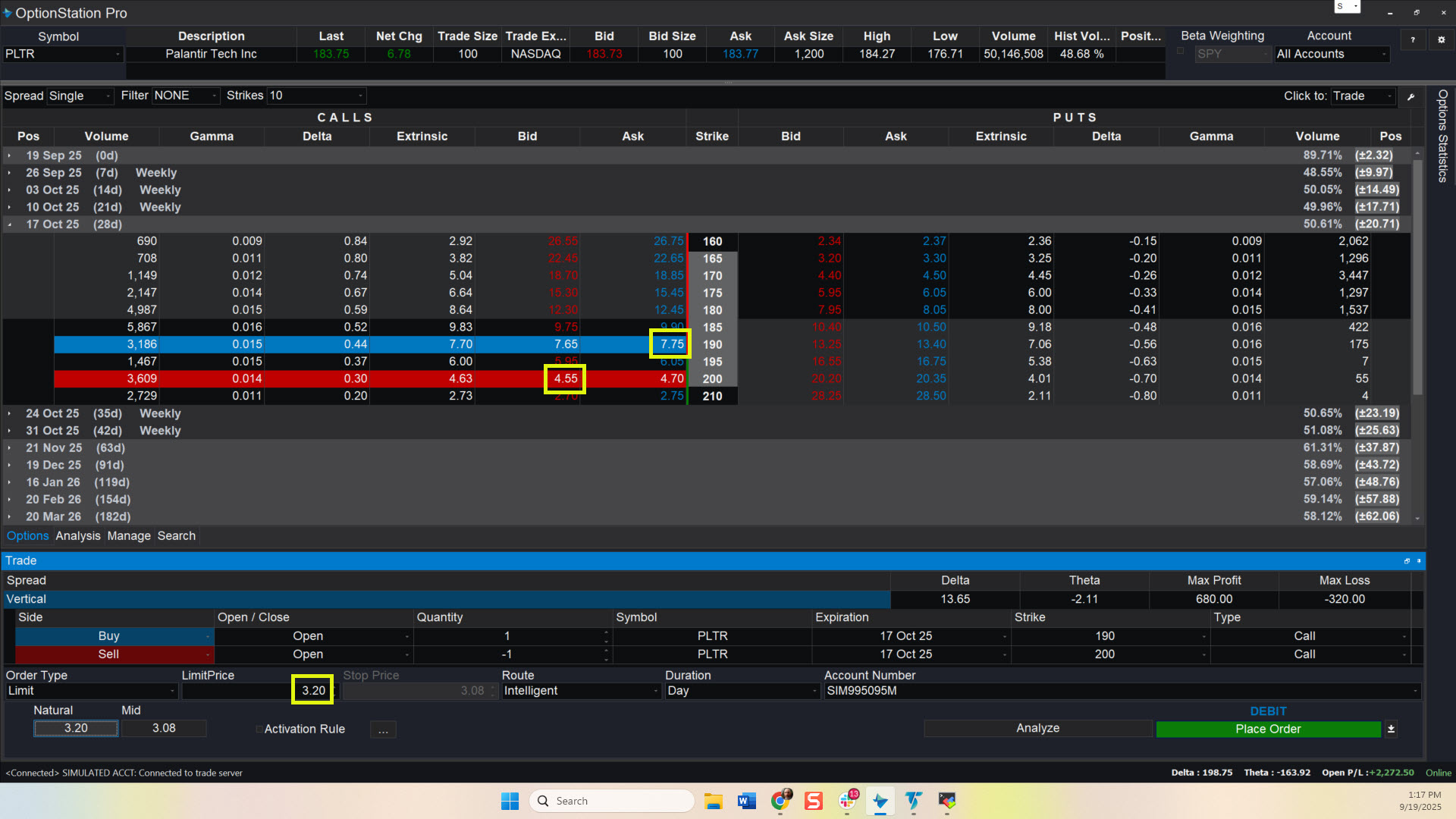

We’ll take as an example Palantir Technologies (PLTR), one of the busiest names in the options market. It was trading around $183.75 on Friday afternoon.

Say an investor thinks it might surpass its August high around $190 and rally above $200 in the intermediate term. He or she might consider a bullish vertical call spread using the standard monthly contracts expiring on October 17, the third Friday of next month.

OptionStation Pro for Palantir Technologies (PLTR), showing the October expiration. Prices cited in this example are marked in yellow.

The October 190 calls were offered for about $7.75 and then October 200 calls had a bid price of about $4.55.

The trader could potentially buy the October 190s and sell an equal number of October 200s for a net cost of $3.20, excluding commissions. (That’s $7.75 minus $4.55.)

The position will have a maximum value of $10 if PLTR closes at $200 or higher on expiration. That’s a potential profit of about 212 percent from the stock moving about 9 percent. The spread will expire worthless if the software company stays below $190. Its breakeven is at $193.20.

Example of a Bearish Vertical Spread

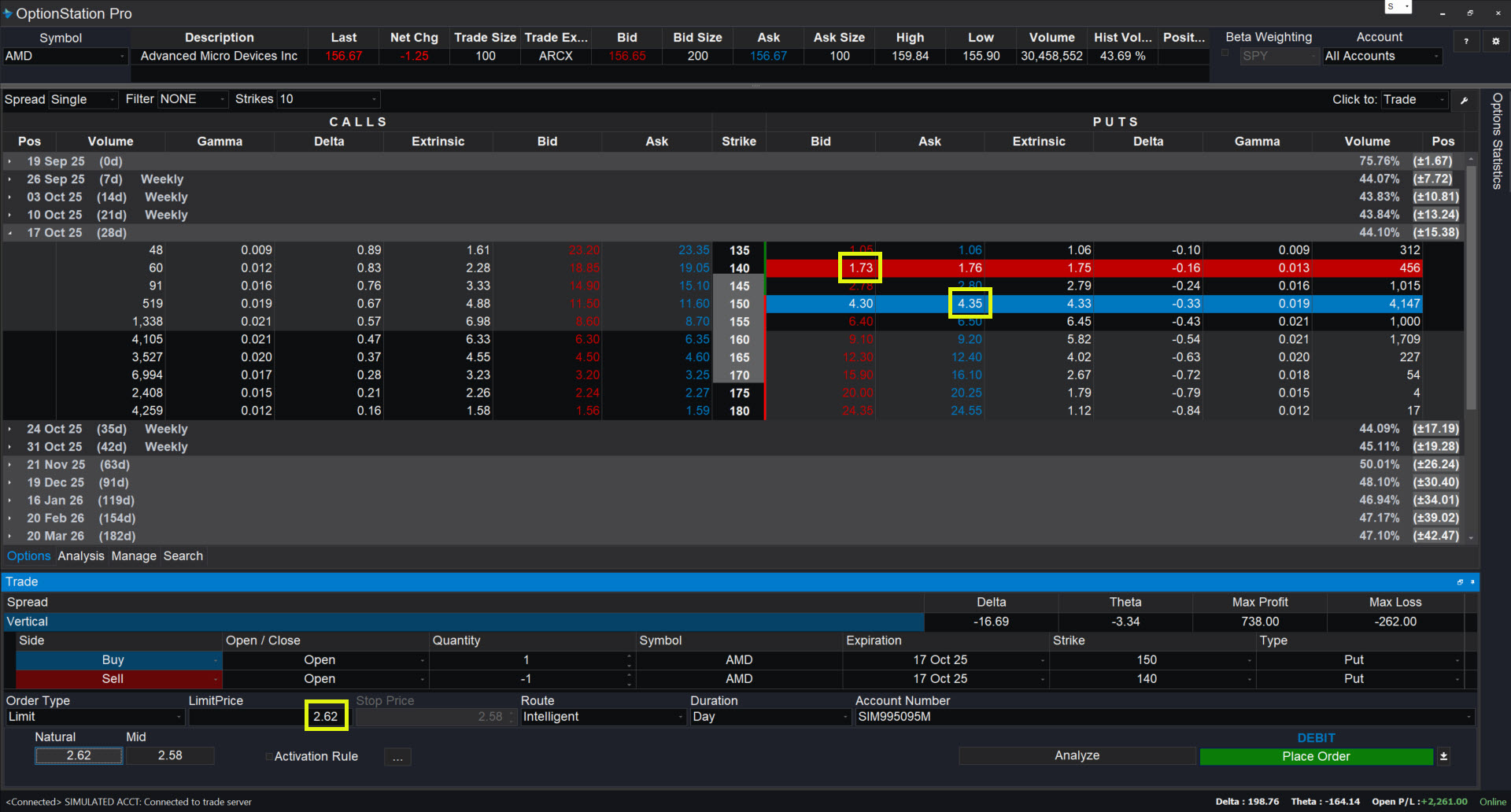

Advanced Micro Devices (AMD), another highly active name, could be considered for a potentially bearish trade. It was trading around $156.67 on Friday.

Say an investor sees risk of it breaking $150 over the intermediate term. He or she might seek a bearish vertical put spread using the standard monthly contracts expiring on October 17.

The October 150 puts were offered for about $4.35 and the October 140 puts had a bid price of about $1.73.

OptionStation Pro for Advanced Micro Devices (AMD), showing the October expiration. Prices cited in this example are marked in yellow.

The trader could potentially buy the October 150s and sell an equal number of October 140s for a net cost of $2.62, excluding commissions. (That’s $4.35 minus $1.73.)

The position will have a maximum value of $10 if AMD closes at $140 or lower on expiration. That’s a potential profit of 282 percent from the stock moving 11 percent. The spread will expire worthless if the semiconductor stock remains above $150. Its breakeven is at $147.38.

Cost Management with Vertical Spreads

Buying a higher-cost option and selling a lower cost option reduces the cost of the overall position. The lower cost can then increase leverage from prices moving in the intended direction.

Traders may use vertical spreads for “binary events” like earnings, when stocks could make sudden moves from one session to the next. They can generate large gains on a percentage basis, profiting from potential moves at a low cost. This reduces the amount of capital investors need to to risk.

Hedging is another potential use of vertical spreads. An investor could own a stock facing a potentially risky event like earnings. They might not want to sell, especially because they think it might jump on the news. He or she might consider buying a put spread below the current price. It could profit from a drop with limited cost, protecting against a decline while letting them benefit from a potential rally.

Limitations of Vertical Spreads

Vertical spreads have some potential drawbacks.

First, vertical spreads realize their full profit potential only close to expiration. If the stock moves in the intended direction, the option sold short will gain value as well as the option purchased. As a result, traders may need to wait for time decay to erode the value of the short leg. It may be difficult to exit quickly.

Second, vertical spreads have limited profits. If prices move move above the higher strike in a bullish trade, the spread’s width caps its potential value. Owning shares or simple calls, on the other hand, have infinite potential upside. (But shares and simple calls also have more risk because they cost more.)

In conclusion, vertical spreads can be a useful strategy for traders to have their toolkit. They can profit from potentially sharp moves around big events with limited risk. Traders can also use them to hedge existing stock positions. However they may require longer hold periods to realize the full gain.

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com/DisclosureOptions. Visit www.TradeStation.com/Pricing for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

ID 4838246